Most companies do not process payments entirely by themselves. The payment ecosystem is complex: there are banks, card networks, fraud checks, regulations, refunds, saved cards, and many operational details that need to work together for a customer to pay successfully.

A payment service provider, or PSP, helps merchants accept payments without having to build all that infrastructure from scratch. Instead of connecting directly to every bank, card network, and payment system, the merchant integrates with one provider and uses its APIs and tools to process payments.

For most companies, starting with a single PSP is the right choice. At the beginning, the problem is simple: the company needs customers to pay, and it needs that to work quickly. A single provider gives the team a practical way to start selling without turning payments into a large internal platform project.

For a while, this model works well. The architecture is simple, ownership is clear, and the product team can focus on growth.

As the company grows, the role of the PSP changes. What began as a convenient integration slowly becomes a critical dependency in the revenue path. Every payment depends on that provider being available and performing well. At the same time, payment fees become harder to ignore. A cost that looked small when volume was low can start taking a meaningful part of the revenue once the business is processing millions in payments.

Higher payment volume usually leads to a different question: how can the company make payment processing more reliable and more cost-efficient?

Reliability means customers should be able to pay when they want, even if the main provider is having problems. Cost-efficiency means the business should not send every payment through the same provider by default if another provider can process that payment with better terms or better results.

Sometimes the best route is the most reliable provider at that moment. Sometimes it is the provider with the best approval rate. Sometimes it is the one with the most favorable cost for that transaction. A multi-PSP architecture gives the company the option to make those choices.

The hidden cost of PSP-owned tokens

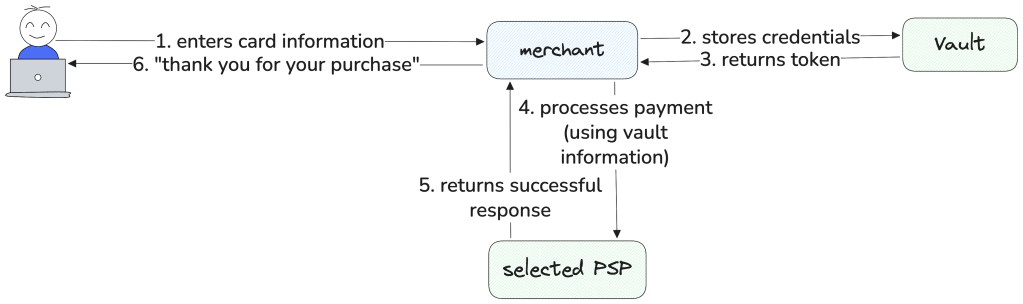

Starting with one PSP is practical, but it also means the first provider often becomes the place where customer payment credentials are stored.

When a customer pays through a PSP, the PSP stores the sensitive card data and gives the merchant a token representing that saved payment method. The merchant can use that token later for saved cards or recurring payments. This is convenient because the merchant avoids handling raw card data directly, but it also means the provider holds that critical information.

If the stored cards were created while the company was using a single PSP, those credentials may not be usable by a new PSP introduced later. The company may add a second provider and still discover that it can only use it for new payments, or for flows where the customer enters the card again. For subscriptions and returning customers, the multi-PSP strategy is limited by where the credentials live.

This creates a form of vendor lock-in. The company is not only dependent on the original PSP for processing. It also depends on that provider for access to the stored payment credentials needed to process future payments. That weakens resilience and reduces commercial leverage, because moving volume away from the original PSP becomes harder.

A stronger long-term design separates the vault from the processor. Instead of storing credentials only inside one PSP, the merchant uses a separate vault and forwards payment requests to the provider selected by the platform.

The details of vaulting, tokenization, and compliance can become complex, but the architectural idea is simple: the payment platform should not be forced to use a specific PSP just because that PSP holds the credential. If the merchant controls the vaulting layer, it has more freedom to route payments based on health, cost, and performance.

What multi-PSP makes possible

Once the company can send the same payment flow to more than one provider, the architecture opens several possibilities. These are not steps that every company must follow in order. They are different ways to take advantage of the optionality created by a multi-PSP setup.

Resilience: keeping payments available

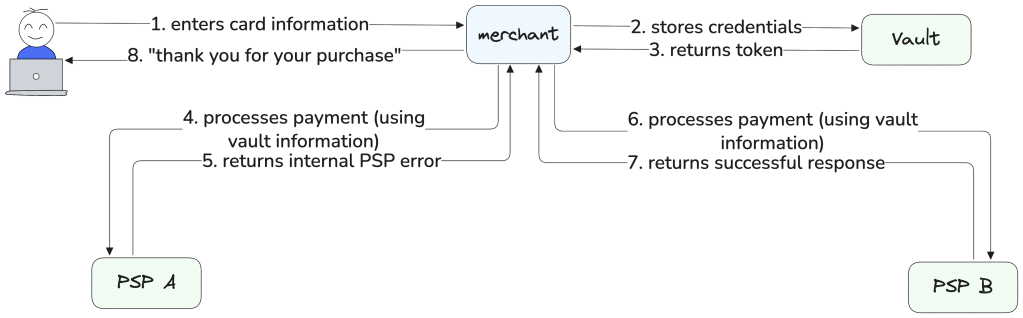

Resilience is usually the first benefit people look for. If PSP A is unavailable, slow, or degraded, the platform can send eligible payments to PSP B. This reduces the risk of having the whole payment flow depend on a single provider. A provider incident no longer needs to become a full payment outage for the business.

Fallback in payments must be controlled. A timeout from PSP A does not always mean the payment failed. It may mean the platform does not know the final state yet. Sending the same payment to PSP B without safeguards can create duplicate charges. A good fallback strategy distinguishes between technical errors, provider degradation, issuer declines, invalid requests, and fraud rejections. The value is not in retrying everything elsewhere, but in knowing which payments are safe and useful to reroute.

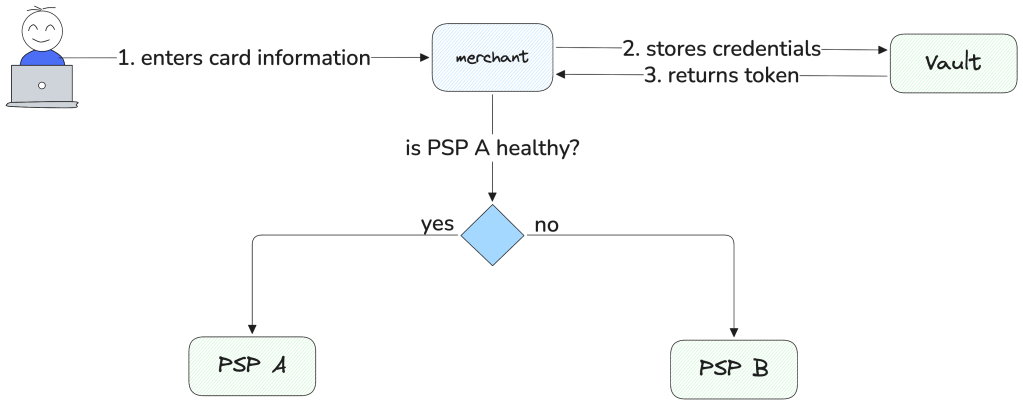

A more advanced resilience strategy is to detect health issues before each payment fails. Instead of waiting for an error and then deciding whether to retry with another PSP, the platform can monitor the main provider and shift eligible traffic when it starts showing signs of degradation. This reduces the chance of customer-facing errors, avoids some of the risk around retrying unknown payment states, and can also improve performance by sending payments through a provider that is responding better at that moment.

This is not trivial to get right. The platform needs to distinguish between a real provider degradation and a normal amount of failed payments. A few declines or timeouts should not automatically move traffic away from a PSP. At the same time, waiting too long can expose more users to a bad payment experience. Health checks, metrics, thresholds, and circuit breakers need to be tuned carefully. The goal is to react fast enough to protect customers, but not so aggressively that the platform starts moving traffic because of noise.

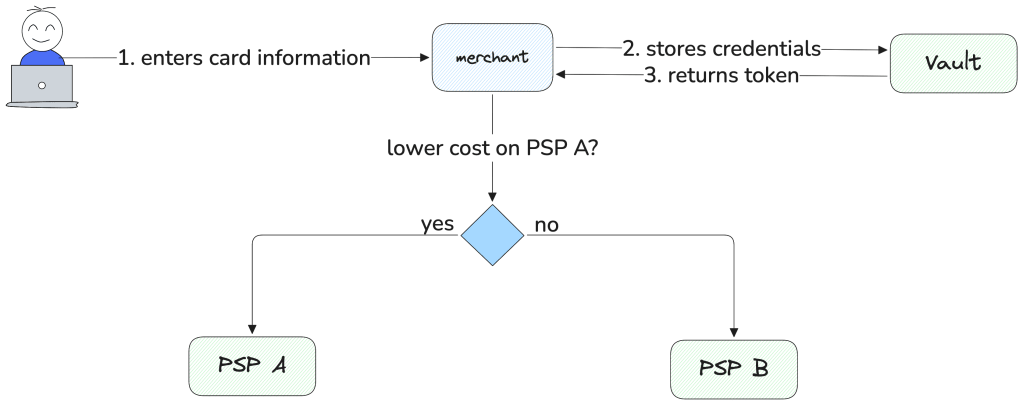

Cost: routing where terms are better

Cost often becomes the next concern. PSPs may offer different commercial terms depending on transaction type, region, card brand, currency, or committed volume. A deal with PSP A may make it cheaper for one group of payments, while PSP B may be more attractive for another. Once more than one provider can process the same payment flow, the company can route payments based on the actual cost of each option instead of sending all traffic through the original integration.

The same idea can be applied beyond cost. It also becomes a way to decide which provider should process each payment. The company can decide where payments should go based on provider health, cost, approval rate, card type, currency, or commercial agreement. The same card payment can be routed differently depending on which provider is expected to produce the best outcome.

Performance adds another dimension. Providers do not behave the same across all traffic. One may have better approval rates for a specific card brand, issuer group, country, or transaction type. Another may have lower latency or fewer technical errors for the same segment. With only one PSP, the company can observe these patterns but has limited ability to act. With multiple PSPs, it can test, compare, and gradually route traffic based on measured outcomes.

Suppose one provider has better pricing for a group of transactions, while another has a higher approval rate. The cheapest provider is not always the most profitable one. If lower fees come with more failed payments, the business may save on processing costs while losing more revenue in failed purchases. A useful routing strategy needs to look at the full outcome: cost, approval rate, reliability, and the value of the transaction.

Routing needs observability

These possibilities only work if the platform can measure what is happening. Without observability, routing becomes guesswork.

A multi-PSP platform needs to compare providers across useful dimensions: approval rate, cost per successful payment, latency, timeout rate, technical error rate, fallback success rate, and performance by country, card, currency, or payment type. The metrics also need to be normalized, because PSPs do not use the same response codes or failure categories.

This is especially important when routing decisions affect money. Looking only at fees, approval rate, or latency can lead to the wrong decision. The platform needs enough visibility to understand how those numbers work together, and whether the routing decision is actually helping the business.

The routing logic should also be explainable. If a payment goes to a specific PSP, the platform should be able to say why. Without this visibility, routing becomes a hidden rules engine that is hard to debug and hard to trust.

The tradeoff with multi-PSP

A multi-PSP architecture gives the company more control, but it also makes the payment platform harder to operate. Each new provider adds another integration to maintain, another set of response codes to normalize, another reporting format to reconcile, and another source of edge cases during incidents.

That complexity is easy to underestimate. A second PSP does not only affect the payment request itself. It affects monitoring, customer support, finance operations, refunds, saved payment methods, incident response, and the way teams reason about payment failures. When something goes wrong, the question is no longer only “did the payment fail?” It becomes “which provider handled it, why was it routed there, what state does that provider report, and what should we do next?”

This is why multi-PSP should not be treated as a maturity badge. For some businesses, a single PSP may remain the best architecture for a long time. The extra complexity only starts to pay off when the cost of dependency becomes higher than the cost of operating multiple providers.

At scale, that tradeoff can change quickly. A provider outage can mean meaningful revenue loss. Small differences in approval rates can become expensive. Processing fees can take a visible share of revenue. Commercial leverage matters more when payment volume is high. In that context, optionality is not just an architectural preference. It becomes a way to protect revenue and improve the economics of the payment flow.

Maximizing the value of PSP relationships

A mature multi-PSP platform is not defined by the number of providers it has. It is defined by how well the company can use those providers.

The point is not to add complexity for its own sake, but to get better returns from each PSP relationship. Those returns can come from higher resilience, better approval rates, lower processing costs, stronger negotiating leverage, or the ability to shift traffic when a provider is not performing as expected.

A single PSP is a good starting point because it keeps the early architecture simple. But as volume grows, the question changes from “Can we process payments?” to “Are we processing payments through the best available route?”

For companies operating at scale, this flexibility matters. Payment providers are not just technical dependencies; they are commercial partners in the revenue flow. A multi-PSP architecture helps the company use those partnerships more intentionally, sending traffic where it creates the most value while avoiding the kind of dependency that turns a provider problem into a business problem.